Billionaire Bill Ackman believes that three Magnificent 7 names are trading below their fair value as investors chase plays widely seen as beneficiaries of the massive AI CapEx.

The News

In a new interview with the All-In Podcast crew, the Pershing Square Capital Management founder says investors have been focusing on the AI picks-and-shovels plays, but they are missing the bigger picture.

“What’s interesting about markets is that people always bring their eyes to the new thing. And the new things are chips, semiconductors and energy. And that’s where the shorter-term capital is going. What tends to happen is that really high-quality things get left behind.

I was there in 2000 in that bubble. This is different, but there are some analogies. And the analogies are that people got excited about internet stocks, and Berkshire Hathaway traded at the lowest valuation I think it ever traded at in its history, as people said, ‘Okay, that’s all old stuff.’

I think a similar thing is happening today, in a sense, to Amazon, Meta and Microsoft. These are old-fashioned companies in this OpenAI era… Yes, [they are undervalued].”

To drive his argument, Ackman says tech giants like Microsoft are in a position to charge less per seat to customers than other software companies.

“If you’re a software company today, you have to be as AI-enabled as you can. I think there has been a monopolistic type of profit-taking off of customers. When someone has a niche software product, they’re charging $30,000 a year or something. I think those companies are really at risk.

Microsoft, when the average customer’s paying $50 a seat or some small number, that platform’s worth a lot more and is less at risk.”

What It Means for Investors

In Q1 of this year, Ackman’s Pershing Square accumulated over $2 billion worth of Microsoft (MSFT) shares while holding other hyperscaler names such as Amazon (AMZN), Meta (META) and Alphabet (GOOGL/GOOG).

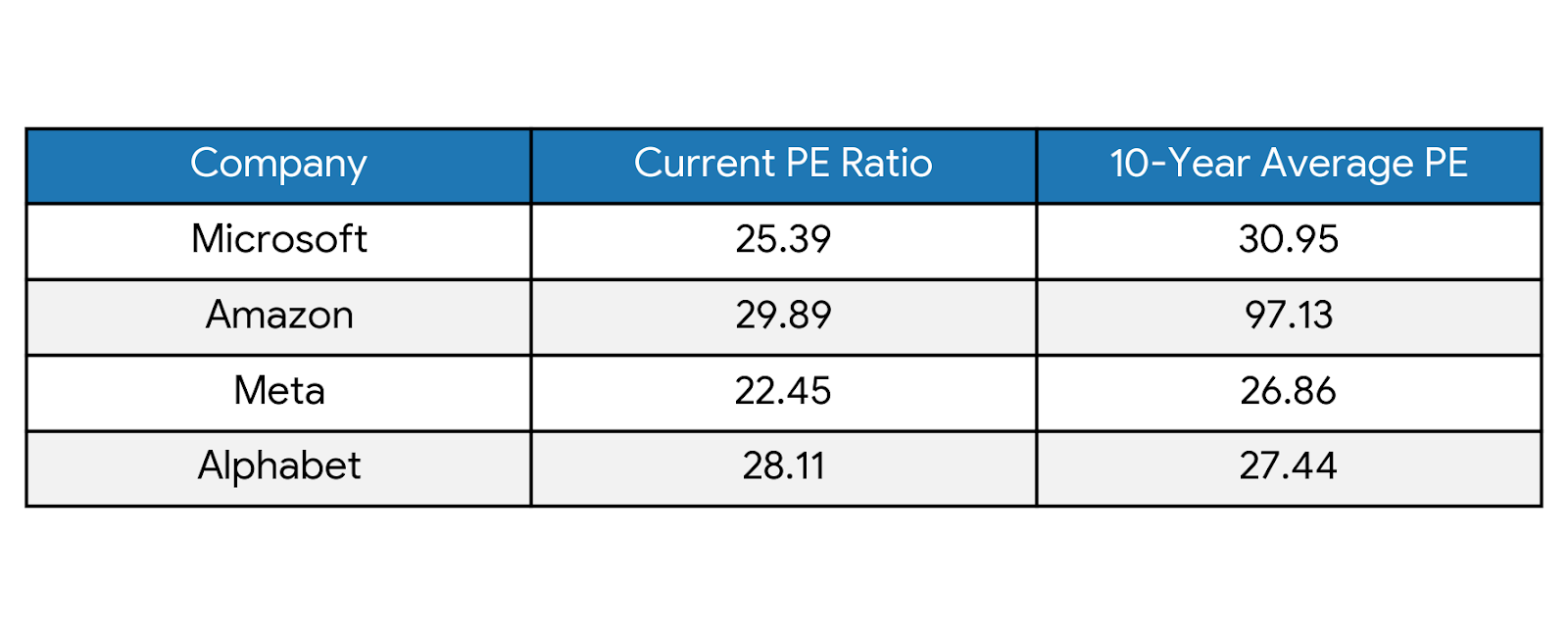

Starting with Microsoft, data shows that its current price-to-earnings (P/E) ratio stands at 25.39, well below its 10-year average of 30.95. Meanwhile, Amazon’s PE ratio of 29.89 is 69% below its 10-year average of 97.13, Meta’s 22.45 PE ratio is 16% lower than its 10-year average of 26.86 and Alphabet’s PE ratio of 28.11 is just slightly higher than its 10-year average of 27.44.

On top of historical valuations, BlackRock CIO Rick Rieder said that the Mag 7 names are “throwing off” 30%-40% earnings growth.

The fundamentals largely support Ackman’s stance that the old-fashioned Magnificent 7 stocks are undervalued.

Ackman is known for making counterintuitive and highly contrarian bets. In 2007-2008, he made a $1.4 billion profit after betting against municipal bond insurers amid the height of the Great Financial Crisis. In 2020, he turned a $27 million credit default swap (CDS) investment into a $2.6 billion payout after correctly predicting that the Covid-19 pandemic would hit the debt markets harder than expected.

If Ackman is right again, the investors flocking into semiconductors and energy may look back at Amazon, Meta, and Microsoft at current valuations the same way Berkshire Hathaway buyers looked back at 1999, wishing they had seen the writing on the wall.

Disclaimer: Opinions expressed at CapitalAI Daily are not investment advice. Investors should do their own due diligence before making any decisions involving securities, cryptocurrencies, or digital assets. Your transfers and trades are at your own risk, and any losses you may incur are your responsibility. CapitalAI Daily does not recommend the buying or selling of any assets, nor is CapitalAI Daily an investment advisor. See our Editorial Standards and Terms of Use.