Investors")

Micron (MU) investors may be facing one of the biggest questions in the AI trade: whether surging demand for memory chips can keep justifying the stock’s explosive rally.

The News

In a new episode of the bank’s Thoughts on the Market podcast, Morgan Stanley head of Europe and Asia technology research Shawn Kim says the memory market is forecast to surge from $220 billion in 2025 to about $890 billion in 2026, a near-quadrupling fueled entirely by AI infrastructure.

“Expectations for 2026 memory revenues rose 71% in just three months. That implies roughly $600 billion of incremental memory revenues in 2026, more than the annual market for smartphones, PCs, or servers, each taken on its own.”

According to Kim, demand is being driven by high-bandwidth memory (HBM) as AI models become increasingly memory-hungry.

“A newer AI chip uses seven times more HBM than earlier generations. A full system uses about 65 times more. Across an entire AI datacenter buildout, the jump gets even bigger. HBM has gone roughly from 10 terabytes in 2020 to about 18 petabytes in 2026, orders of magnitude more. This demand is running into a supply chain that cannot respond quickly.”

What It Means for Investors

The HBM market is dominated by three players: SK Hynix, Samsung and Micron. Among the three, only Micron is a direct US-listed play, which largely explains why MU is up nearly 190% year-to-date.

According to Kim, demand for HBMs exploded by 1,800x in just six years. While he did not get into the specifics driving growth, UBS hinted that structural changes in AI are the catalyst propelling the demand explosion.

The structural change is the way AI models process data nowadays. Back then, models typically answered user queries with internet text. Earlier AI workloads were more heavily associated with training and text generation. Today, more investor attention is shifting toward inference, where deployed models process prompts, retrieve context, reason through tasks and generate outputs at massive scale.

This is where Micron’s HBM3E comes into play, as it is designed to deliver speed, capacity and power efficiency, all of which are ideal for AI inference.

The data shows that the inference market is poised for massive growth in the coming years.

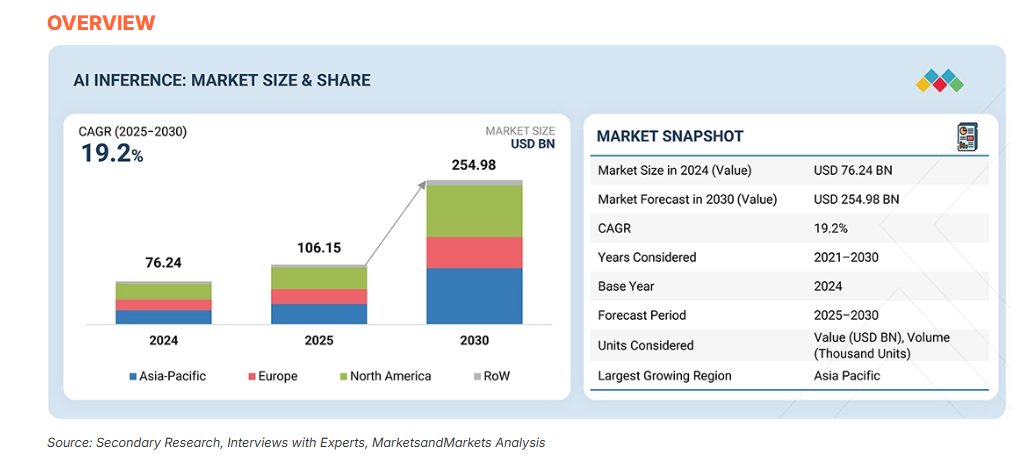

What the Data Says

The data on the total addressable market (TAM) for fast inference varies. The intelligence platform MarketsandMarkets forecasts the TAM for AI inference surging from $106.15 billion in 2025 to $255 billion in 2030.

Meanwhile, Barclays analyst Tom O’Malley predicted that the TAM could reach $300 billion by 2030, and Mizuho projects aggressive growth to $550 billion by the end of the decade.

Institutional investors are positioning to capture the upside potential. Billionaire Ray Dalio’s Bridgewater Associates owns nearly $500 million in MU shares, while billionaire Paul Tudor Jones holds $120.091 million worth of MU shares as of Q1 of 2026.

The Bear Case

MU is slated to release its fiscal third-quarter 2026 earnings report on June 24th, 2026. In its fiscal Q2, Micron saw its revenue climb about 200% to $23.86 billion. The firm has previously guided for revenue to hit $33.5 billion in fiscal Q3.

The firm’s valuation is also stretched, with a price-to-earnings ratio of 44.23 compared to its historical average of 19.48 and the tech sector’s average of 36.32.

MU’s daily chart also shows a bearish divergence on the relative strength index (RSI), suggesting that buying momentum is slowing even though price continues to climb. The stock’s RSI has also dropped below 70, indicating a loss of momentum. In technical analysis, the signals suggest that a correction or a consolidation is in sight.

Investor Takeaway

The data shows that long-term structural tailwinds support Micron’s growth, but the market ebbs and flows, and MU is not immune to that cycle. Citi Research global head of technology and communications Heath Terry said that dips are for buying. If he’s correct, the price action before and after MU’s June 24th report could open opportunities for long-term investors and dip buyers.

Disclaimer: Opinions expressed at CapitalAI Daily are not investment advice. Investors should do their own due diligence before making any decisions involving securities, cryptocurrencies, or digital assets. Your transfers and trades are at your own risk, and any losses you may incur are your responsibility. CapitalAI Daily does not recommend the buying or selling of any assets, nor is CapitalAI Daily an investment advisor. See our Editorial Standards and Terms of Use.